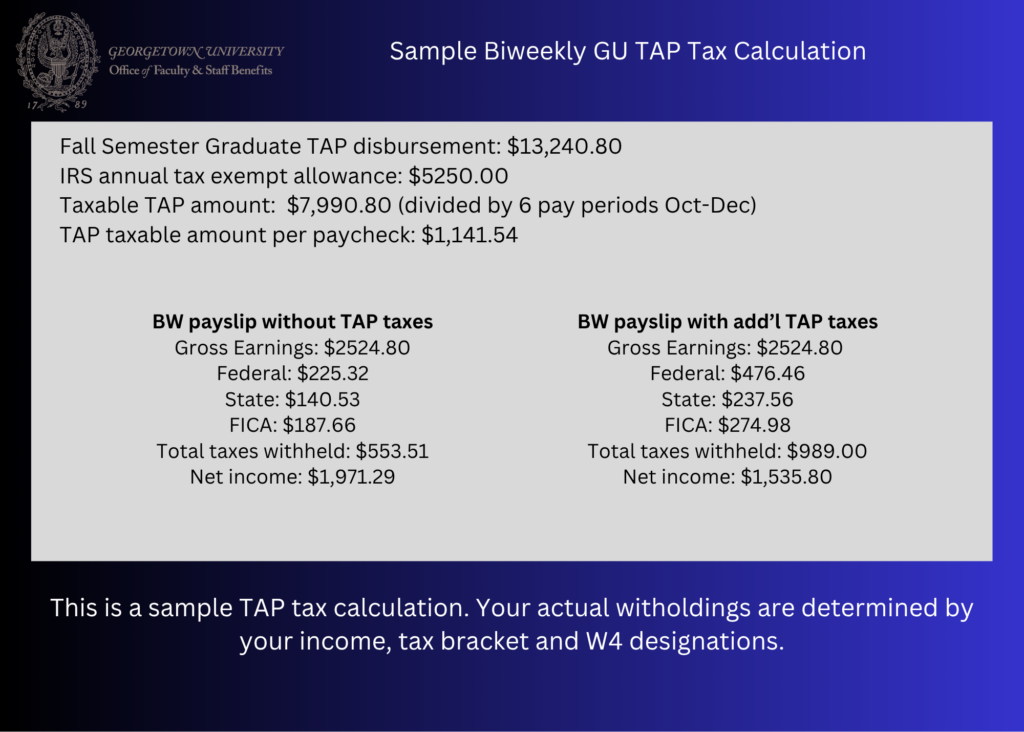

The Georgetown University Tuition Assistance Program (TAP) benefit is automatically taxable at the federal and state level when applied to graduate level courses. A number of factors influence the tax calculation, including income, tax bracket and designations on your Federal and local withholding form. We recommend that you consult with a tax advisor to determine the impact on your income and plan accordingly for any additional tax withholding before financially committing to your program.

Tax Withholding Schedule

- Fall semester: October-December

- Spring Semester: February-May

- Summer Semester: June-August

Taxability Table

| Eligible TAP Recipient | Taxability of GU Non-Credit Certificate | Taxability of GU Undergraduate Enrollment | Taxability of GU Graduate Enrollment | Taxability of Non-GU (External) Graduate Enrollment |

|---|---|---|---|---|

| Active Employee, self-use | Exempt | Exempt | Exempt up to $5,250 per calendar year – Excess included in gross wages and taxes will be withheld* | N/A – except legacy TAP recipients |

| Active Employee, Child use | N/A – Benefit not provided | Exempt | When eligible, full TAP value included in gross wages and subject to tax withholding | N/A – Benefit not provided |

| Retiree, self-use | Exempt | Exempt | Exempt up to $5,250 per calendar year. Retiree TAP reported as earnings on W2 and subject to tax withholding | Exempt up to $5,250 per calendar year. Retiree TAP reported as earnings on W2 and subject to tax withholding |

| Retiree, Child use | N/A – Benefit not provided | Exempt | When eligible, full value reported as earnings on W2 and subject to tax withholding | N/A – Benefit not provided |

*Active employees may request a review to determine if eligible for tax free treatment. For planning purposes, the University can provide a provisional tax exempt determination prior to your acceptance in a graduate program. Never assume you will qualify for tax free treatment – always anticipate added tax withholding on your earnings.

Please read the Tuition Remission Tax Liability policy for a better understanding of the review process.

In accordance with IRS guidelines, tuition benefit tax exemption might apply if:

- The graduate education improves the skills required of the employee in their current job;

- The graduate education is not a requirement in the current HR position description; and

- The education does not prepare the employee for a new career.

The process for determining tax exempt TAP benefits requires submission of a “tax free” request package, including your official Human Resources GU Position Description obtained from your department or your HR Business Partner.

TAP Tax Exempt Review Process

In order for Georgetown University to properly administer tax-exempt TAP benefits in accordance with IRS requirements, we will require specific information from employees who are enrolled in graduate programs.

Your submission of a TAP tax-exempt request package is reviewed and a determination will be made confirming whether or not your education qualifies for tax free treatment under IRC 132(d) as a Working Condition Fringe Benefit. All determinations are final and not subject to appeal. Remember, GU TAP benefits used for graduate studies are automatically taxed unless you are provided with a written determination to the contrary.

The following steps are required in order to submit your tax-exempt request package

- STAFF: We require a copy of your formal GU Position Description (an HR document) – please obtain it in advance to aide in completing this request.

- FACULTY: a copy of your CV and contract must be uploaded with this request in lieu of a human resources GU Position Description.

- Step 1: ALL APPLICANTS: Complete this Google Form. Be prepared to upload the GU Position Description (or Faculty CV) into this form where instructed.

- Step 2: ALL APPLICANTS: Complete and sign the separate Word addendum, obtain your supervisor’s signature, and upload into this form where instructed.

Submission Deadlines

- Spring Semester: December 1

- Summer Semester: June 1

- Fall Semester: August 1

If you have any questions, please contact the Office of Faculty and Staff Benefits by emailing tapbenefits@georgetown.edu.